Introduction to Equilibrium in Economics

Equilibrium in economics is one of the most fundamental concepts in economic theory. It refers to a situation where economic forces such as demand and supply are balanced, resulting in stability in the market. At equilibrium, buyers and sellers are satisfied with the prevailing price and quantity, and there is no tendency for change unless external factors disturb the market conditions.

The concept of equilibrium serves as the foundation of both microeconomics and macroeconomics. Economists use equilibrium analysis to understand how markets function, how prices are determined, and how resources are allocated efficiently. Whether studying consumer behavior, production decisions, national income, or international trade, the idea of equilibrium plays a central role.

In modern economies, equilibrium helps explain the interaction between consumers, producers, governments, and international markets. Understanding equilibrium enables policymakers, businesses, and individuals to make informed economic decisions. It also provides valuable insights into market efficiency, economic growth, inflation, unemployment, and resource allocation.

Meaning and Definition of Equilibrium in Economics

The term “equilibrium” originates from the Latin word aequilibrium, meaning balance. In economics, equilibrium refers to a state where opposing forces are equal and there is no incentive for change.

Market Equilibrium

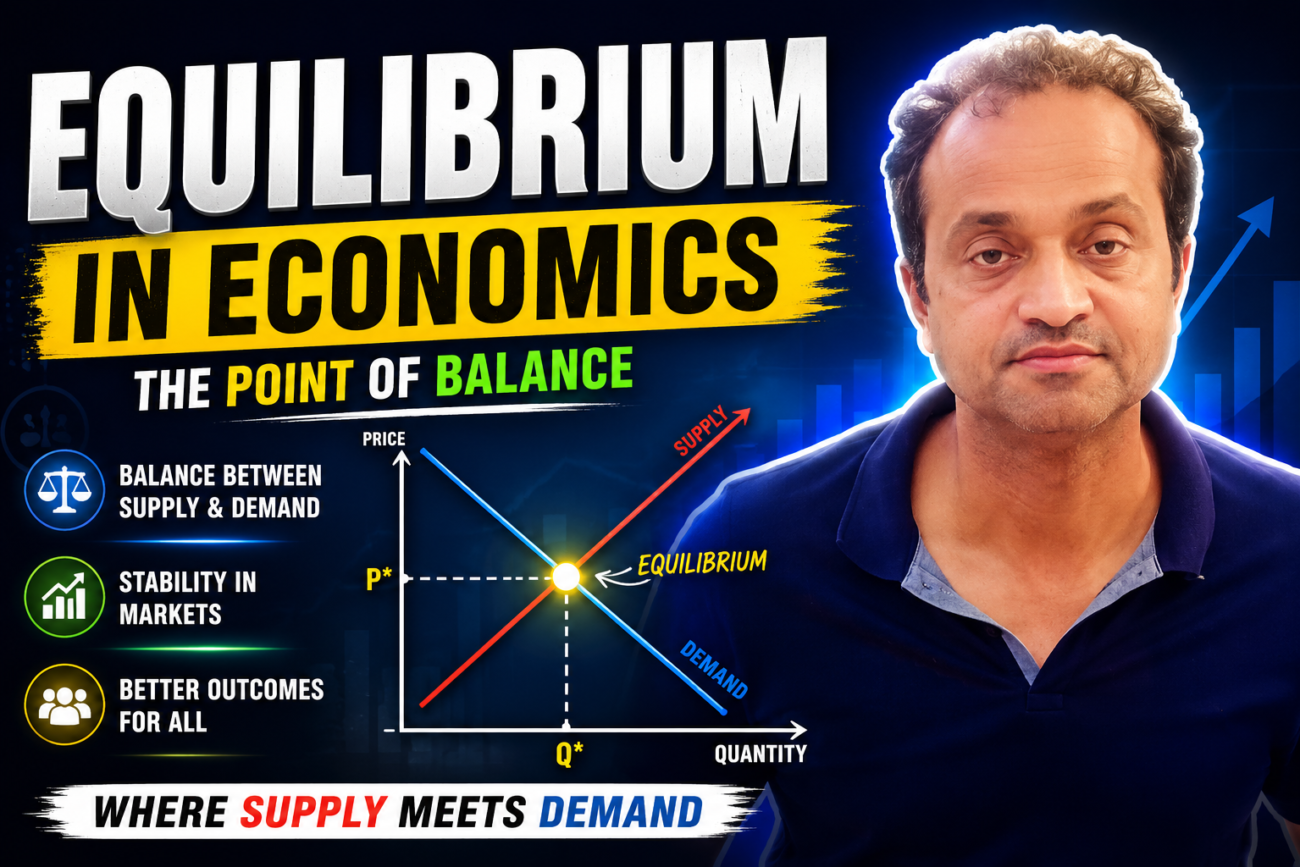

Market equilibrium occurs when the quantity demanded by consumers equals the quantity supplied by producers.

Q_d = Q_s

At this point:

- There is no shortage in the market.

- There is no surplus in the market.

- Market price remains stable.

- Buyers and sellers are satisfied.

- Resources are allocated efficiently.

The price at which demand equals supply is known as the equilibrium price, while the corresponding quantity is known as the equilibrium quantity.

For example, if consumers are willing to purchase 1,000 units of a product at ₹100 and producers are willing to supply exactly 1,000 units at the same price, the market is said to be in equilibrium.

Historical Development of Equilibrium Theory

The concept of equilibrium has evolved significantly throughout the history of economics.

Classical Economists

Classical economists such as Adam Smith believed that markets naturally move toward equilibrium through the invisible hand mechanism. They argued that competition among buyers and sellers ensures efficient resource allocation.

Neoclassical Economists

Economists such as Alfred Marshall further developed equilibrium theory by introducing demand and supply analysis. Marshall’s work established the foundation of modern market equilibrium.

General Equilibrium Theory

Léon Walras introduced the concept of general equilibrium, emphasizing that all markets in an economy are interconnected. Changes in one market can affect equilibrium in others.

Today, equilibrium analysis remains a central component of economic research and policy formulation.

Demand and Supply: The Foundation of Equilibrium

Understanding equilibrium requires a clear understanding of demand and supply.

Demand

Demand refers to the quantity of goods and services consumers are willing and able to purchase at various prices during a given period.

Factors affecting demand include:

- Income levels

- Consumer preferences

- Population growth

- Prices of related goods

- Future expectations

Supply

Supply refers to the quantity of goods and services producers are willing and able to offer for sale at different prices.

Factors affecting supply include:

- Production costs

- Technology

- Government policies

- Resource availability

- Market expectations

The interaction between demand and supply determines market equilibrium.

Equilibrium Price and Equilibrium Quantity

The point where demand and supply curves intersect represents equilibrium.

P_e

The equilibrium price is the market-clearing price where buyers and sellers agree on transactions.

Characteristics of equilibrium price:

- No excess demand

- No excess supply

- Efficient allocation of resources

- Market stability

Similarly, equilibrium quantity represents the amount bought and sold at equilibrium price.

Businesses closely monitor equilibrium quantity because it indicates the optimal production level required to satisfy market demand.

Types of Equilibrium in Economics

Economists classify equilibrium into several categories.

1. Stable Equilibrium

Stable equilibrium occurs when the market automatically returns to equilibrium after a disturbance.

For example, if prices temporarily rise above equilibrium, excess supply develops. Producers reduce prices, bringing the market back to equilibrium.

Stable equilibrium is commonly observed in competitive markets.

2. Unstable Equilibrium

Unstable equilibrium occurs when disturbances push the market further away from equilibrium instead of restoring balance.

In such situations, small changes may create large fluctuations in prices and quantities.

3. Neutral Equilibrium

Neutral equilibrium exists when disturbances neither restore nor move the system further away from equilibrium.

The market simply settles into a new position.

4. Partial Equilibrium

Partial equilibrium examines a single market while assuming all other markets remain unchanged.

Examples include:

- Wheat market equilibrium

- Automobile market equilibrium

- Smartphone market equilibrium

5. General Equilibrium

General equilibrium studies the entire economy simultaneously.

It considers interactions among:

- Consumers

- Producers

- Labor markets

- Financial markets

- Government sectors

General equilibrium provides a broader understanding of economic activities.

Dynamic and Static Equilibrium

Static Equilibrium

Static equilibrium assumes economic variables remain unchanged over time.

The economy is analyzed at a specific point without considering future adjustments.

Dynamic Equilibrium

Dynamic equilibrium recognizes that economic variables continuously change while maintaining overall balance.

Modern economies often experience dynamic equilibrium because technology, preferences, and policies constantly evolve.

Disequilibrium in Economics

Disequilibrium occurs when demand and supply are not equal.

Excess Demand

When quantity demanded exceeds quantity supplied:

- Shortages arise.

- Prices increase.

- Producers expand output.

Excess Supply

When quantity supplied exceeds quantity demanded:

- Surpluses develop.

- Prices decline.

- Producers reduce production.

Market forces typically eliminate disequilibrium and restore equilibrium over time.

Importance of Equilibrium in Economics

Equilibrium plays a vital role in economic analysis.

Efficient Resource Allocation

Equilibrium ensures resources are allocated to their most productive uses.

Price Determination

Market equilibrium helps determine fair prices for goods and services.

Economic Stability

Balanced markets reduce uncertainty and encourage investment.

Consumer Satisfaction

Consumers obtain desired products at acceptable prices.

Producer Efficiency

Businesses can optimize production and maximize profits.

Policy Formulation

Governments use equilibrium analysis when designing fiscal and monetary policies.

Equilibrium in Perfect Competition

Perfect competition provides the classic example of market equilibrium.

Characteristics include:

- Large number of buyers and sellers

- Homogeneous products

- Free market entry and exit

- Perfect information

In perfect competition, firms accept the market price determined through demand and supply interactions.

Long-run equilibrium occurs when:

- Firms earn normal profits.

- No new firms enter the market.

- Existing firms have no incentive to leave.

This situation promotes economic efficiency and consumer welfare.

Equilibrium in Monopoly Markets

A monopoly exists when a single firm dominates the market.

Unlike competitive markets, monopolies determine output and prices strategically.

Monopoly equilibrium occurs when:

- Marginal Revenue equals Marginal Cost.

MR = MC

Monopolists typically charge higher prices and produce lower quantities than competitive firms.

As a result, market efficiency may decline.

Equilibrium in Macroeconomics

Macroeconomic equilibrium refers to balance within the entire economy.

It involves variables such as:

- National income

- Employment

- Inflation

- Investment

- Consumption

Income-Expenditure Equilibrium

Macroeconomic equilibrium occurs when planned expenditure equals national output.

Where:

- Y = National Income

- C = Consumption

- I = Investment

- G = Government Spending

- X = Exports

- M = Imports

This equilibrium determines overall economic activity.

Equilibrium and Consumer Behavior

Consumers constantly make choices regarding consumption.

Consumer equilibrium occurs when individuals maximize satisfaction given their income constraints.

According to utility theory, equilibrium is achieved when:

- Marginal utility per rupee spent is equal across all goods.

Consumer equilibrium helps explain purchasing decisions and market demand patterns.

Equilibrium and Producer Behavior

Producers seek profit maximization.

Producer equilibrium occurs when firms choose production levels that maximize profits.

This generally happens when:

- Marginal Cost equals Marginal Revenue.

At this point:

- Profits are maximized.

- Production efficiency is achieved.

- Resources are utilized effectively.

Role of Government in Maintaining Equilibrium

Governments often intervene to maintain economic equilibrium.

Methods include:

Fiscal Policy

Governments adjust:

- Tax rates

- Public spending

- Budget deficits

Monetary Policy

Central banks regulate:

- Interest rates

- Money supply

- Credit availability

Price Controls

Governments may impose:

- Price ceilings

- Price floors

While intended to stabilize markets, excessive intervention may sometimes create disequilibrium.

Real-World Examples of Equilibrium

Housing Market

Housing prices adjust based on demand and supply.

When demand exceeds supply, prices rise until equilibrium is restored.

Labor Market

Wages are determined through interaction between labor demand and labor supply.

Equilibrium wages balance employment opportunities and workforce availability.

Agricultural Markets

Crop prices fluctuate according to production levels and consumer demand.

Equilibrium ensures efficient distribution of agricultural products.

Financial Markets

Stock prices move toward equilibrium based on investor expectations and available information.

Challenges to Achieving Equilibrium

Several factors can disrupt equilibrium:

- Inflation

- Economic recessions

- Technological changes

- Government regulations

- Natural disasters

- Global trade shocks

- Political instability

Modern economies constantly adjust to these challenges while seeking equilibrium.

Equilibrium in the Digital Economy

The rise of digital platforms has transformed traditional equilibrium analysis.

Online marketplaces use real-time data to adjust prices dynamically.

Examples include:

- E-commerce platforms

- Ride-sharing services

- Online advertising markets

- Streaming subscriptions

Technology enables markets to reach equilibrium more rapidly than ever before.

Conclusion

Equilibrium in economics is a cornerstone of economic theory and practice. It represents a state of balance where demand equals supply, resources are allocated efficiently, and markets operate smoothly. From consumer decisions and business strategies to government policies and global trade, equilibrium influences virtually every aspect of economic activity.

Understanding equilibrium helps explain how prices are determined, why markets fluctuate, and how economies achieve stability and growth. Whether studying microeconomics, macroeconomics, international trade, or financial markets, equilibrium remains an indispensable analytical tool. As economies continue to evolve through technological innovation and globalization, the concept of equilibrium will remain essential for understanding and managing economic systems in the modern world.